Charging Infrastructure Part 3: Competitive Dynamics

EVgo believes it has a business with a moat - does it?

Welcome to Efficiencies, a blog situated at the intersection of strategy and sustainability, exploring all that relates to the business models and industry dynamics of the disruptors and the disruptees in our shift to the Green Economy. If you like what you read, please show your support with a free subscription or by sharing with a friend! Join the discussion and let’s grow this community.

This is part 3 and the conclusion of the series on fast charging infrastructure! Having covered both the cost side (in part 1) and the revenue side (in part 2) of charging infrastructure, the natural question is now how much revenue, and therefore profit, can a single fast charger capture? An interesting claim EVgo’s management makes is that investors should compare its charging assets to communication infrastructure companies like AMT, CCI and SBA. These companies have high cost leverage, growing demand but limited growth in towers, a recipe for great ROE which investors will refer to as a “moat” and pay rich multiples for. If the fast charging market is conducive to moats and EVgo is really the next AMT (with higher growth to boot), then EVgo is substantially mispriced. Is it?

The Competitive Environment

One of the first lessons in economics is about market structures. If you are buying lemons for $1/lb and selling them for $2/lb, then I might like to steal your customers by selling lemons for $1.90/lb and making a profit of $0.90/lb. Of course, you might retaliate by lowering your price. Then a third party (let’s call it Life) may come in and sell lemons for $1.70/lb because it’s still profitable. This would continue until we were all selling lemons at a price where our return on assets just covered our cost of capital. That’s what we call a perfectly competitive market. All markets gravitate towards this state unless there is something that allows one or some parties to protect their profits – if the product is differentiated, if the business has a network effect or if there are barriers to entry, for example.

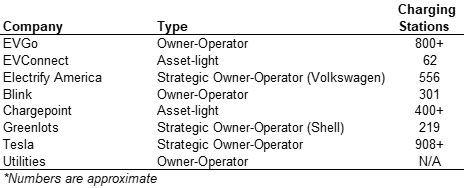

Competitors in the fast charging market fall into owner-operators, strategically owned owner-operators and asset light operators categories.

If you consider the incentives of the various types of competitors, they’re all incentivized to overbuild - not exactly a moat-like characteristic. The primary product for the strategic owners (aside from Greenlots-Shell) is electric vehicles – they want people to feel comfortable purchasing EVs, not maximize their profit margin. Tesla runs its fast charger network at breakeven. Asset-light operators have a distorted incentive. Chargepoint will sell a fast charger and supporting software subscriptions to its customers; it has no exposure to the amount of electricity sold or a unit’s profitability and so is incentivized to sell as many fast chargers as possible.

Owner-operators are incentivized by subsidies and short-term demand charge holidays to build as quickly as possible in the near-term. Utilities, who manage the electric grid and must invest in additional infrastructure to support fast chargers added to its network, are the only ones who could be interested in controlled growth. However, there’s nothing from the utilities that suggests they are concerned about the rate of fast charger growth.

EVgo in context

If you take the 112 GWh of fast charging demand in 2019 and spread it over the 3,701 fast chargers in the U.S., EVgo’s average of .02 GWh sold per charger in 2019 is only slightly below the market average of .03 GWh. That’s actually not bad considering the vast majority of electric vehicles on the road were sold by Tesla, who operates its own fast charging network. It speaks to the site selectiveness of EVgo’s management - per Bloomberg:

“The company prefers to position chargers in clusters around higher traffic regions, as opposed to long strands of plugs that would help shrink charging deserts but get less use. In some parts of the country, EVgo said it can’t build chargers fast enough. “We’re barely skating ahead of the puck,” said Julie Blunden, EVgo’s executive vice president of business development.

The companies use rate is high because it has skipped over much of the country. “What we won’t do is build willy-nilly and then wait three years for demand to show up,” Blunden said. Population density, the number of nearby EV owners and traffic at existing EVgo stations dictate where new chargers will go.”

As we’re presently in no danger of having a long-term oversupply of fast chargers, there’s a slight upside to being an owner-operator. Strategically owned owner-operators and asset-light operators have different priorities. Asset-light operators are indifferent to where their fast chargers go, since their revenues are not tied to utilization, and fast charging networks controlled by automakers are interested in assuaging would-be EV owner range anxiety, not maximizing returns. As the same article points out:

“Because Tesla CEO Elon Musk is more interested in selling vehicles than electricity at charging stations, his plugs are scattered more widely around the country. For example, Wyoming has 10 Tesla charging stations but only one fast-charging plug suitable for a Jaguar I-Pace. West Virginia is a little more balanced; it has eight Tesla stations and two fast-charging spots for other EVs.”

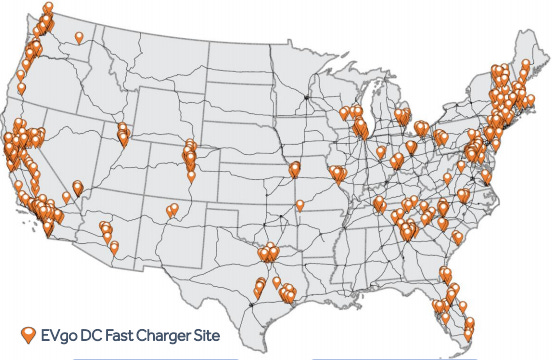

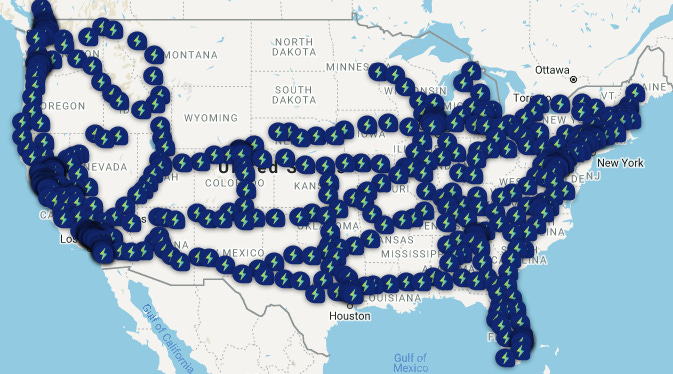

It's plausible to imagine a scenario where EVgo, as the largest non-strategic owner-operator, cultivates a portfolio of high return locations and automaker-owned fast charging networks fill in the less attractive gaps. Automaker controlled fast charging networks have, in fact, followed a different approach than EVgo by focusing on highways and corridors. Compare EVgo’s charger map with Volkswagen-owned Electrify America:

The differing priorities between EVgo and the automakers raises some question about EVgo’s contract with GM to bring 2,750 chargers to its network - will it require them to build in less desirable locations?

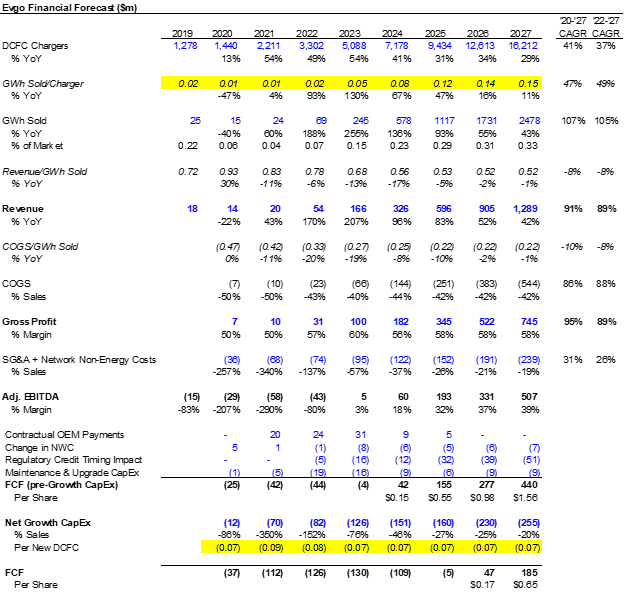

It would be illuminating (albeit wishful thinking) if management provided a more granular breakdown of its utilization and the attractiveness of the top 100 MSAs based on available subsidies/rate structure and expected EV growth. Yet it’s obvious when you look at the embedded assumptions in EVgo’s financial forecast that they expect to build in dense, high-traffic areas in states with generous subsidies:

Note the 47% CAGR in per charger GWh sold (a proxy for utilization expectations), which comes on top of the 41% CAGR in chargers. What stands out to me is the implied capex per new DCFC; a single 150 kW DCFC charger costs between $75-100k before factoring in development and installation costs1, yet EVgo expects to pay only $70k per new charger added to its network.

In truth, the fast-charging market is an amalgamation of hyperlocal markets; having a dominant presence in Los Angeles has no bearing on how well a network competes two hours away in San Diego2. That’s part of what makes it so difficult for this kind of business to have a moat, but also part of what makes it difficult to make a summary judgement on the competitive landscape. Any investor with ~$300k can purchase a ChargePoint fast charger and enter a suburban market with high utilization, but in dense urban areas with aged electrical infrastructure and limited room to build you could make a case for barriers to entry. Consumer decisions for a commoditized product like electricity are based on convenience and price; there’s no brand loyalty to keep the new entrant from siphoning off business.

But how many fast chargers do we need in the mid-term?

It’s unlikely that the fast charging business has a moat, but high growth markets can ignore that for a time as competitive forces take a backseat to rapid demand growth. There are currently ~17k fast chargers in the U.S., or one per 59 BEVs given an estimated 1 million VIO (Vehicles in Operation). It’s difficult to draw a direct comparison with gas stations when estimating how many fast chargers the market needs; you can charge your EV at home but you need to go to the gas station to refuel your car, for example. Loren McDonald does the math in this old CleanTechnica article and comes up with a reasonable estimate of 225 gas cars per gas pump. Applying this ratio to EVgo’s forecast for 4m electric VIO in 2025 implies demand for ~18k fast chargers, a little more than we currently have today. But an important distinction to make is that over half of these fast chargers are owned by Tesla and service only Tesla vehicles – with other automakers stepping up their EV commitments, the actual base of fast chargers available to service their customers is under 8k. If non-Tesla automakers sell 2 million BEVs between now and 2025, then the gas station ratio implies demand for ~10k DCFC chargers.

Personally, I suspect the ratio of electric cars to fast chargers will be lower than the gas station ratio given lower turnover (it takes 5 minutes to refuel a tank, but 30-60 minutes to recharge a battery) and the smaller range of EVs that is further depleted by accessories like air conditioning. For reference, China has a ratio of 12:1 EVs to fast chargers while California set a target of 10k fast chargers in 2018 and today is projected to need 25k fast chargers by 2030 to support its target 5 million electric VIO.

Conclusion

Competitive dynamics are less punitive in markets with significant whitespace for businesses to expand into. The deployment of EVs – particularly fleet EVs – will be far more consequential in the near and mid-term. EVgo is an interesting competitor in this landscape whose incentives are most closely aligned with cultivating an efficient charging network and capitalizing on available subsidies/partnerships to do so. In the short-run, this combination of demand growth and subsidies will inflate EVgo’s ROE – although whether there are enough possible locations with California-level support for EVgo to 8x its network at a consistent IRR is something only management knows. In the long-run, this is not a market where EVgo can easily defend its returns. It is not an AMT, but it is a compounder. You just may not want to pay 23x EBITDA for it3.

The NYT cites a $1m estimate all-in cost for a fast charging station from the Rocky Mountain Institute

Also recall from part 1 that utility cost structures, regulations and government support can vary significantly from market to market, exacerbating the heterogenous nature of the national market

AMT’s forward EV/EBITDA multiple; definitely not investment advice