Charging Infrastructure Part 2: Electric Boogaloo

Charging Infrastructure Part 2: Electric Boogaloo

Part 2 of our series on EVgo & charging infrastructure takes a look at the drivers of market demand

Efficiencies is a blog situated at the intersection of strategy and sustainability, exploring all that relates to the business models and industry dynamics of the disruptors and the disruptees in our shift to the Green Economy. If you like what you read, please consider a free subscription or sharing with a friend! Join the discussion and let’s grow this community.

Last week’s article introduced EVgo, the leading owner-operator of fast charging stations, which offers a unique way for investors to play the electric vehicle megatrend and claims it can reach unit economics of >30% IRR. Part 1 focused on the cost side of fast charging stations and the particular challenge posed by utilities rate structures. As an aside, I had an intense feeling of déjà vu when I saw this story come out from Greentech Media:

To recap Part 1, demand charges, which are set based on the peak power output in the billing cycle, create unfavorable economics for fast chargers, which are characterized by low utilization punctuated by spikes in output. Many utilities and states have proposed holidays from demand charges; this flatters unit economics in the near-term and contributes to management’s forecast for 30% IRRs and 61% adjusted EBITDA margins. But costs are only part of the equation. This week in part 2 we evaluate the market opportunity.

The Fermi Technique

One of my favorite things to do is to test the assumptions in management presentations. Far too often analysts will accept management math without question because it looks professional and it answers a question that seems hard to answer ourselves. What is the future demand for fast charging?

Usually, management is working with data not much better than what we can access on the internet but they always have an incentive to present their business case in the most favorable light. So it is always worthwhile to do your own market forecast, if just to better understand the assumptions underlying management’s.

For this, I love the Fermi technique. Enrico Fermi was a physicist known for his ability to make good approximate calculations with little or no actual data. A Fermi estimate typically involves decomposing the original problem into smaller problems that are easier to solve. If anyone has asked you how many piano tuners there are in Chicago and stepped you through estimating the population of Chicago, how many families own a piano, the frequency of piano tuning… that’s the Fermi technique. It’s also referred to as “back-of-the-envelope” math or guesstimating. I like to call it ballparking.

Ballparking Fast Charging’s Addressable Market

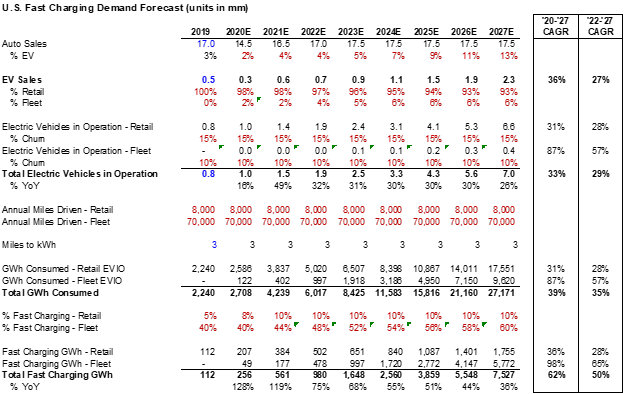

The addressable market for fast charging is a function of electric cars on the road (i.e. electric vehicles in operation or VIO), how many miles they’re driving and how many of those miles are charged at fast charging stations. What type of electric car matters as well, since fleet cars, from uber drivers to amazon delivery vans, and medium heavy duty (MHD) vehicles drive more miles than retail.

This is how I roughly ballparked demand (assumptions are in red, known data in blue and formulas in black):

As this is for illustrative purposes, I’m not accounting for the dip in miles driven caused by COVID or a possibly permanent impairment caused by increased remote work. I would encourage further refinement for more serious analysis (feel free to reach out to me on Twitter @AmbroseKira or email for the model and play around with the assumptions), but this is a good starting point. Two things immediately stand out to me:

First, my estimate is much smaller than the market presented by management. I’m in line with management on electric VIO - the difference stems from assumptions on how many fleet EVs are sold and how many miles are charged through fast charging.

Second, fleet adoption of EVs really is key to the EVgo investment thesis. These vehicles drive multiple more miles than retail and because they’re operating a business, they will use fast chargers more frequently to get back on the road.

So, where are fleet vehicles coming from?

There were a few electric fleet announcements tucked into the wave of sustainability announcements over the last 12 months. President Biden pledged that the federal government’s fleet of vehicles, which numbered 645k as of 2019, will transition to fully electric. Amazon has a purchase order for 100k EVs. These seem like small numbers in the context of the +270m vehicles in operation in the U.S., and especially considering the timeline; Amazon’s fleet will have 10,000 EVs by 2022 and 100,000 by 2030 while Biden has yet to provide details for the electrification of the U.S. fleet. The truth is the chicken-or-the-egg problem that hindered EV adoption hasn’t fully gone away. EV fleet customers require infrastructure to purchase EVs, infrastructure requires customers to continue adding charging stations and OEMs require demand to manufacture EVs. Amazon’s order, the company notes, is the largest ever for electric delivery vans. That and orders from the U.S. government are meant to be the first move that gets the cycle going, a promise of volume that allows the other two players to invest in the necessary manufacturing capacity and infrastructure that will in turn enable demand. Current demand is being met by startups such as Rivian (in which Amazon owns a stake) and GM’s BrightDrop, who are still building up production capacity. For this reason I think it’s hard to get too bullish in the near term – customer growth is a real constraint in terms of the capacity to produce fleet EVs and, more broadly, the available supply of batteries.

Lyft and Uber, by virtue of using passenger electric vehicles, are a more promising source of near-term electric fleet growth with over ~2 million combined vehicles. Both businesses have pledged to electrify their fleets but, since they do not ultimately own the cars in their networks their efforts are limited to incentivizing drivers. Lyft summarized their electrification commitment as follows:

“We expect our path to follow a 3-step plan: (1) focus on policies to accelerate EV cost-parity, (2) lead with Express Drive EV rentals to provide nearer-term EV access, and (3) build demand for EVs among millions of Lyft platform users, including rideshare drivers, riders and transportation managers. By starting with electrification of rental vehicles available through Express Drive, we plan on leveraging our purchasing power to negotiate pricing and deliver cost savings to our customers using that program. We expect to be able to electrify Express Drive rental partner vehicles sooner than drivers will shift to electric with personal vehicles because Express Drive vehicles drive more miles per year on average than personal vehicles, and hence can recoup a higher upfront vehicle cost through faster fuel and maintenance savings that are accrued on a per-mile basis.

We expect to begin ramping up acquisition of EVs for the Express Drive rental partner program over the next five years and shift all new vehicle acquisition to 100% EV beginning in 2026. And we expect to achieve 100% electric miles driven by Express Drive vehicles in 2028. For drivers’ personal vehicles, we expect the cost of EVs to continue to decrease – through more cost-effective battery and hydrogen fuel cell technology and policy support for vehicle purchasing and charging, among other things – so that drivers using personal vehicles will begin significantly ramping up adoption of EVs by 2026.”

This touches on a crucial point – adoption is ultimately tied to economic incentives, especially commercial (fleet & MHD) EV adopters who must deal with disadvantageous range and refilling times versus a gas engine. I’ve written before that most consumer don’t realize the cheaper total cost of ownership of EVs because most electric cars are leased and savings aren’t realized until the seventh or eighth year of ownership. It’s no accident that EVgo’s charger map reflects the states that most heavily incentivize electrification:

Notably, I’ve left out MHD vehicles in my forecast. This is where I think management is a touch optimistic. Unlike last-mile fleet vehicles that have short routes and frequent stops, Medium duty trucks are typically used to transport goods or people between cities within the same state; once the weight of cargo is factored in the economics fall apart. Per Goldman Sachs,

“Based on annual cost savings estimates of $10,000 per year and a premium of $60,000 for an electric truck in 2025 with a 500-mile range1, truckers who are not constrained by weight would achieve a 6-year payback period, significantly longer than the 2-year payback that over the road truckers typically target… If weight is a constraint, electric trucks are not viable, in our view. The revenue shortfall of $26,000 per year significantly outweighs the maintenance and fuel cost savings of $10,000 per year, meaning a payback is never achieved.”

Summing it all up…

In my mind, the biggest bet you need to make forecasting demand growth for fast charging is on the upfront cost of electric vehicle ownership coming down, likely through government action, since economically-minded commercial vehicles will constitute a disproportionate share of fast charging demand. Any actions from states or the federal government to lessen the upfront cost of passenger and light commercial electric vehicles, or mandate electric MHD vehicles, would dramatically change the outlook for the electric VIO and fast charging demand. Given the increased global urgency around climate change and current administration, I think the risk here skews positively. Secondly, there’s the impact on miles driven from COVID to consider.

On my more modest ballpark math EVgo’s projection for selling 2,478 GWh in 2027 implies a 33% market share (21% on management’s math). That’s highly consolidated for such a nascent, high growth market and begs the question, does this business have a moat?

Coming up in part 3:

The competitive landscape of fast charging infrastructure

Can fast charging infrastructure have a moat?

This is quite optimistic given electric MHDs today have a range of ~100 miles, implying a 5x improvement in 4 years. It also means the payback is even less attractive with lower range vehicles.